Buying a condo in Philadelphia can be a smart way to enjoy city living, build equity, or invest in rental property. Whether you are looking at a luxury high-rise in Center City or a smaller philly condo building in South Philadelphia or Northern Liberties, financing a condo works differently than financing a single-family home.

Lenders do not just evaluate the buyer. They also evaluate the condo building itself, the homeowners association (HOA), reserve funds, insurance coverage, owner occupancy ratios, and even pending lawsuits.

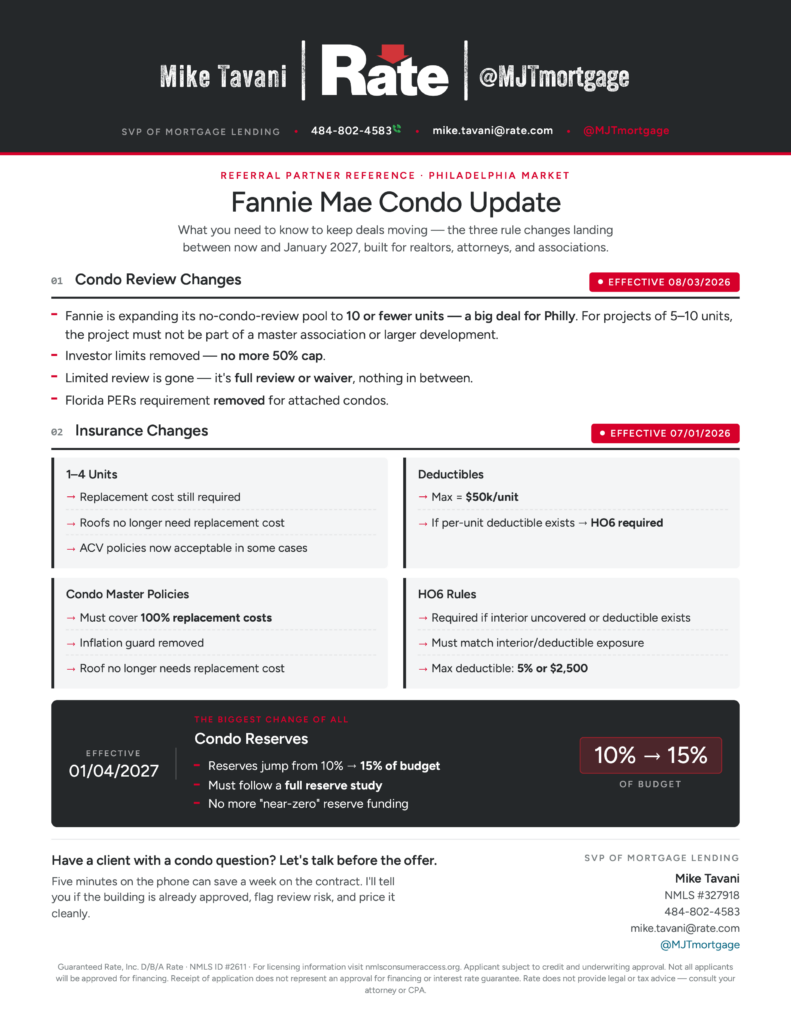

That matters even more now because Fannie Mae is rolling out major condo financing updates between 2026 and 2027 that could directly impact condo buyers, investors, HOA fees, and financing approval timelines.

For buyers searching for a condo in Philadelphia for sale, understanding these financing changes early can help avoid delays, unexpected costs, or financing denials later in the process.

Why condo financing is different from buying a house?

When financing a condo, lenders evaluate both the buyer and the condo association. That is one of the biggest differences compared to buying a traditional home.

For example, lenders may review:

- HOA reserve funds

- Building insurance coverage

- Percentage of owner-occupied units

- Number of investors in the building

- Delinquent HOA dues

- Pending lawsuits

- Future special assessments

- Overall building financial health

This extra review process is why condo loans can sometimes take longer to close and may have slightly higher interest rates. This is especially important in older condo buildings and larger condo developments throughout Philadelphia.

What are the new Fannie Mae loan limits for 2026?

For 2026, conforming loan limits increased again in many markets due to rising home values.

In most areas, the baseline conforming loan limit is expected to remain above $800,000, while high-cost markets may exceed $1 million.

This matters for buyers looking at condos in Philadelphia Center City, where luxury condo prices can quickly move into jumbo financing territory.

Loan limits impact:

- Minimum down payment requirements

- Interest rates

- Mortgage insurance

- Qualification guidelines

Buyers purchasing higher-end condos should confirm early whether the property falls within conventional loan limits or requires jumbo financing.

What Is Changing With Fannie Mae Condo Financing?

Fannie Mae is rolling out several major condo financing changes between 2026 and 2027 that could significantly affect condo buyers, investors, HOAs, and condo associations.

The Biggest Change: Reserve Requirements Increase

One of the largest updates is that condo associations will need to increase reserve funding requirements from 10% to 15% of the HOA budget.

This means:

- HOA fees may increase

- Associations may need reserve studies

- Deferred maintenance may become harder to ignore

- Lenders will review building finances more carefully

Buildings with weak reserve funding could face financing challenges.

Condo Review Rules Are Changing

Fannie Mae is also expanding its “no condo review” eligibility to buildings with 10 or fewer units. This is especially important in Philadelphia, where many boutique condo buildings fall into this category.

Buildings With 10 Units or Less

Requirements are easing for smaller buildings. That could make financing easier and faster for many smaller philly condo projects throughout Philadelphia neighborhoods.

Buildings With More Than 10 Units

Lenders are expected to review larger buildings more closely.

Buyers may see:

- More document requests

- Longer approval timelines

- Higher HOA scrutiny

- Increased insurance review

- Potentially higher fees

This could especially impact larger high-rise condo developments in Center City.

Investor Limits Are Being Removed

Fannie Mae is also removing the old 50% investor concentration cap in some situations. That may improve financing flexibility for some condo investors and mixed-use condo communities.

How Will the New Condo Rules Impact Philadelphia Condo Buyers?

For those looking to buy condo in Philadelphia, these updates create both opportunities and risks.

Buyers in Smaller Buildings May Benefit

Philadelphia has many smaller condo buildings with fewer than 10 units. These buildings may now qualify for simpler financing reviews, making approvals faster and easier.

Larger Buildings May Face More Scrutiny

Buyers in large condo towers may experience:

- Higher HOA fees

- More underwriting conditions

- Insurance-related delays

- Increased reserve funding requirements

This does not mean financing will disappear. It simply means lenders are becoming more cautious about building financial stability.

Which Loan Programs Are Specifically Designed for Condo Buyers?

Several programs are designed to make condo ownership more accessible.

Fannie Mae HomeReady

HomeReady loans help lower-income buyers purchase condos with:

- Low down payments

- Reduced mortgage insurance

- Flexible income guidelines

Freddie Mac Home Possible

This program is similar to HomeReady and allows financing up to 97% loan-to-value.

FHA Loans

FHA loans remain one of the most popular condo financing options for first-time buyers. However, the condo building must appear on HUD’s approved FHA condo list.

VA Loans

VA loans continue to provide one of the strongest financing options for eligible military buyers. The condo project must typically be VA-approved.

What Makes a Condo “Warrantable” or “Non-Warrantable”?

A warrantable condo meets Fannie Mae and Freddie Mac guidelines.

These buildings are easier to finance.

Typical Warrantable Condo Requirements

- Strong reserve funding

- Limited investor ownership

- Adequate insurance

- No major lawsuits

- Low HOA delinquency rates

- Mostly owner-occupied units

Non-warrantable condos may require specialty financing with:

- Higher interest rates

- Larger down payments

- Stricter underwriting

Tips for Getting Approved for a Condo Mortgage in Philadelphia

– Work With Experienced Philadelphia Realtors

Condo financing can become complex quickly. Experienced Philadelphia Realtors can help identify financing risks early.

– Review HOA Documents Before Making an Offer

Do not wait until underwriting to discover reserve issues or pending assessments.

– Get Fully Pre-Approved Early

A strong pre-approval can make your offer more competitive in Philadelphia’s condo market.

– Ask About Building Approval Status

Some condo buildings are already approved with certain lenders, which can simplify financing.

– Budget Beyond the Mortgage

Remember to account for:

- HOA fees

- Condo insurance

- Special assessments

- Parking fees

- Property taxes

FAQ

Is it harder to get financing for a condo in Philadelphia?

Sometimes yes. Lenders evaluate both the buyer and the condo building itself, including HOA finances, reserve funds, and insurance coverage.

What credit score do you need to buy a condo?

Most conventional condo loans require at least a 620 credit score, although FHA loans may allow lower scores.

Can you buy a condo in Philadelphia with 3% down?

Yes. Some conventional programs allow 3% down, while FHA loans allow 3.5% down for qualified buyers.

Why are lenders reviewing condos more carefully now?

Recent Fannie Mae changes increased reserve and insurance requirements due to concerns about deferred maintenance and condo association financial stability.

Are condos in Philadelphia good investments?

They can be, especially in strong rental and walkable neighborhoods. However, investors should carefully review HOA rules, rental restrictions, and building finances before purchasing.

Top real estate agencies specializing in Philadelphia condos

If you’re buying in Society Hill, local expertise matters.

We recommend Venture Philly Group, located right inside Hopkinson House.

Ask for Antonio Atacan—a Society Hill resident with 30+ years of experience who knows every building, rule, and hidden detail.

Disclaimer:

This article was created by real estate professionals for informational and educational purposes only. Financing guidelines, loan requirements, condo approval standards, interest rates, and lending programs can change frequently and may vary based on the lender, building, borrower qualifications, and market conditions. Buyers and investors should always speak directly with a licensed mortgage lender or loan officer to receive the most accurate and up-to-date financing information for their specific situation. This article should not be considered financial, legal, or lending advice.